For construction and trade businesses across Queensland and NSW, June is typically the busiest claims month of the year. Projects are active, progress claims are going out, and the full-year revenue figure will reflect the strongest numbers on the P&L.

The bank account in mid-July will often tell a different story.

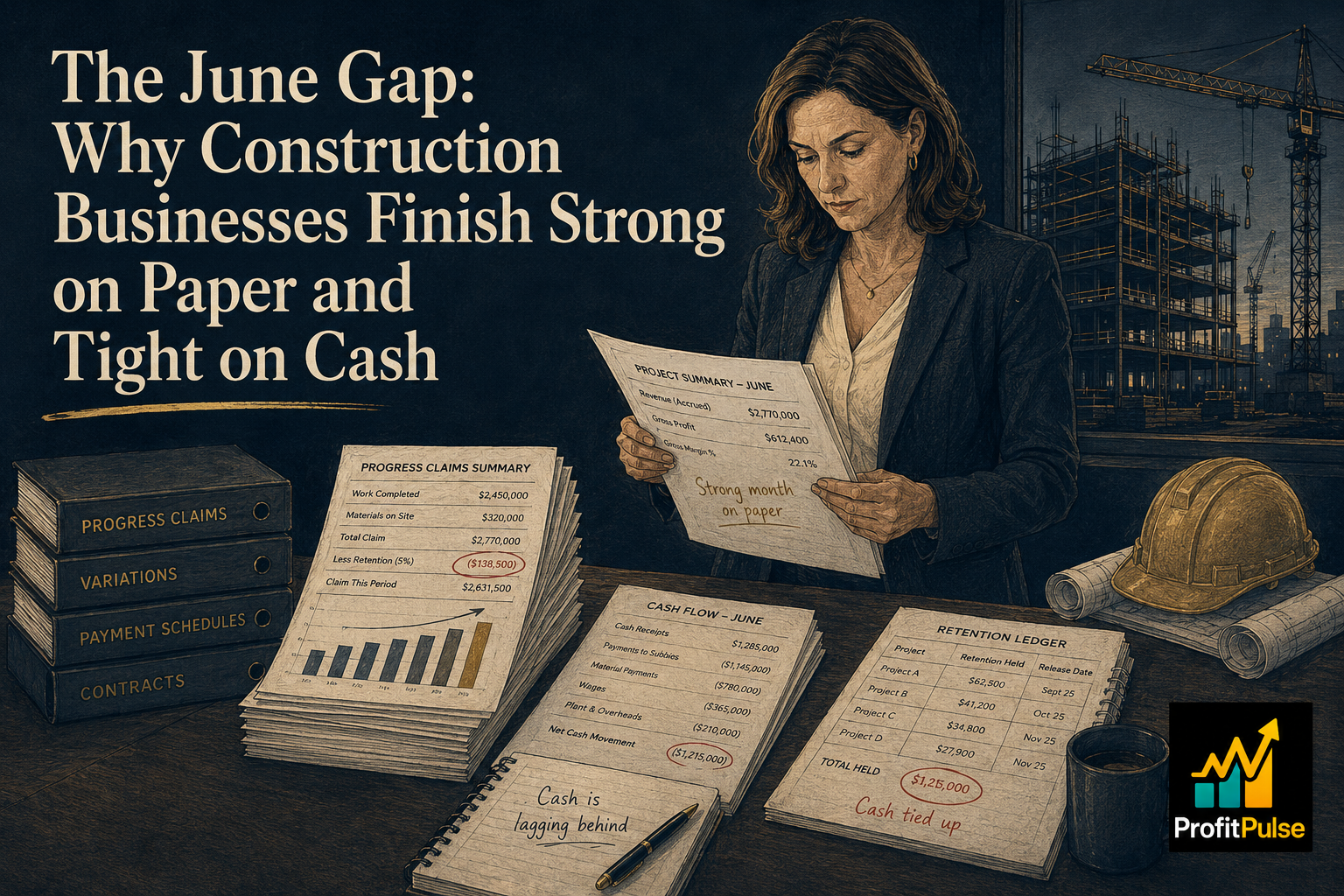

This is the June gap in construction, and it is not the result of poor management or an unusual year. It is the structural outcome of how construction revenue works: retentions held by clients and Work In Progress on active contracts create a consistent difference between what has been earned and what has actually arrived in the account. Both are predictable. Neither, in most construction businesses, gets properly planned for until the pressure is already being felt.

What Retention Is Doing to Your Balance Sheet

On most commercial construction contracts, clients withhold a percentage of each progress claim, typically five to ten percent, until practical completion is certified and the defects liability period expires. This retention money sits in the debtors ledger as a receivable. It looks like money owed. But it cannot be chased the way a normal invoice can.

Retention release is governed by contract conditions and, in Queensland and NSW, by security of payment legislation. Until the project reaches practical completion and the relevant conditions are satisfied, the retention balance is held. For a business with several simultaneous projects, the cumulative retention figure in June can be substantial, and most of it will not land in the account in July.

This matters for two reasons. The first is cash: the business has funded the work that generated the retention, recognised it as revenue, and is now waiting for it to release, sometimes for months. The second is the balance sheet: a lender or buyer reading the year-end accounts will age the retention and discount its quality. A retention schedule that does not document completion status and expected release dates for each project makes the receivables look weaker than the headline total implies.

Before June 30, it is worth identifying which retentions are already legitimately releasable. Projects that reached practical completion and cleared their defects period before June 30 represent real money the business can collect now. A focused review of the retention schedule in the last fortnight of June typically surfaces one or two balances that are already due and have simply not been followed up.

The WIP Position and Its Effect on Cash

Work In Progress is the cost and value of work performed on active contracts that has not yet been invoiced. On a lump-sum or fixed-price contract, it represents the gap between the work completed and the amounts claimed to date.

A business that has billed less than the work completed is under-billing. It has performed the work, carried the cost, and has not yet converted it to a claim. The WIP asset sits on the balance sheet, but the cash to fund it has already left the account. A business that has billed ahead of completion has over-billed. This is not unusual in construction where early milestone billing is common, but it means a portion of the cash received represents work still to be done.

At EOFY both positions have direct consequences. Under-billing means unclaimed revenue is sitting in the project and the business is funding the gap from its own cash. Over-billing means the accounts look strong but a corresponding liability sits against it. Neither is inherently a problem, but understanding which position the business is in before June 30 changes what decisions are available.

A Working Capital Unlock across a construction business maps the retention balance against each project’s completion status, charts the WIP position across active contracts, and produces a prioritised list of where cash is sitting in the cycle and what it takes to release each item. For most businesses that run this exercise, the finding is not one large problem but several smaller ones that have accumulated quietly across the project pipeline.

Planning the July Position Before June 30

The July cash pressure in construction is predictable once the inputs are mapped. Progress claims submitted in June typically settle mid to late July, depending on the contract payment terms. Subcontractor invoices from May and June fall due in the same window. Superannuation for the April to June quarter is payable by 28 July. And for many businesses, the new financial year order book is still converting from quotes while the prior year’s costs continue to land.

Building a 13-week cash flow forecast through June 30 and into September, with the project billing schedule mapped against committed outflows, shows the July position clearly before it arrives. For construction businesses, this is the most actionable use of the fortnight before EOFY: knowing what the account will look like in the third week of July, and having a plan rather than a surprise.

For business owners thinking further ahead, the same project-level data that creates July pressure is the data a buyer will read when assessing the business. A construction business where the retention schedule is clean, WIP is documented by project, and progress billing reflects work completed will present a considerably more transparent picture during due diligence. An Exit Readiness Diagnostic after EOFY, when a full year of project data is available, identifies which of the eight buyer-grade readiness dimensions deserve attention in the years before a planned exit.

ProfitPulse works with construction and trade businesses across Queensland and NSW at this point in the calendar, when the pipeline is active and the financial picture for the full year is taking its final shape. If June revenue looks strong and the July cash position has not yet been mapped against what is coming, that picture is worth building now. Book a complimentary 45-minute discovery call with ProfitPulse.

Frequently asked questions

What is retention in a construction contract and how does it affect my cash flow?

Retention is a percentage of each progress claim (typically five to ten percent) that a client withholds until practical completion and the expiry of the defects liability period. For a construction business with multiple active projects, the cumulative balance can be substantial. It sits in the debtors ledger as a receivable but cannot be collected until the contract conditions are met. A Working Capital Unlock maps each project’s retention balance against its completion status and identifies which amounts are already releasable.

When can I release retention money from a client in Queensland or NSW?

Retention is releasable once practical completion is certified and, where applicable, once the defects liability period has expired. In Queensland and NSW, security of payment legislation provides specific rights to recover retention. On residential projects in Queensland, retention practices differ from commercial construction and are regulated under the Queensland Building and Construction Commission framework. For commercial projects, checking the contract completion trigger before June 30 identifies which retention balances are already due and can be claimed before the financial year closes.

What is construction WIP and why does it matter for my EOFY accounts?

Work In Progress (WIP) is the value of work completed on active contracts that has not yet been invoiced. At EOFY, the WIP position determines how revenue and costs are matched in the accounts. A business under-billing relative to completed work is funding the gap from its own cash. A business over-billing carries a corresponding liability on the balance sheet. Both positions affect the tax outcome for the year and what a lender or buyer reads in the year-end financials.

How should I manage cash flow in my building or trade business in July?

Start with a forward cash flow view that maps outstanding progress claims, expected client payment dates, retentions scheduled to release, and committed outflows. Superannuation for the April to June quarter is due by 28 July. Subcontractor invoices from May and June settle in the same period. Building this picture in the second half of June, before the obligations arrive, gives the business time to arrange facility headroom or accelerate specific debtor collections rather than managing reactively.

What does a buyer look for when valuing a construction business in Australia?

Buyers examine project-level financial records closely: whether WIP is documented by contract, whether the retention schedule shows clear completion status, and whether progress billing is current. Owner dependence, contract concentration, and the business’s ability to deliver without the principal managing every site determine where the multiple lands. An Exit Readiness Diagnostic scores the business across all eight buyer-grade readiness dimensions and identifies which structural changes would most improve the valuation outcome.

Should a construction or trade business owner work with a fractional CFO?

For businesses between three and twenty million in revenue, where the principal is managing project delivery alongside financial administration, a fractional CFO arrangement brings the WIP tracking, retention management, and forward cash flow discipline that construction businesses need but rarely have bandwidth to build themselves. The return typically shows in better billing discipline, earlier identification of project margin issues, and a cleaner balance sheet that supports banking and valuation conversations.

What is a progress claim in construction and how does billing timing affect working capital?

A progress claim is an invoice for work completed to date on a project, submitted in accordance with the contract’s payment schedule. In Queensland and NSW, security of payment legislation provides rights to serve payment claims and recover amounts due within specified timeframes. A business that defers billing until project completion funds all costs from its own cash for the full duration of the contract. Submitting claims at each contractual milestone converts completed work to receivables as quickly as the contract allows.

Leave a Reply