The end of financial year conversation in most owner-led businesses follows familiar territory in June: what did the year deliver, where does the tax position sit, and which spending decisions still make sense before 30 June. These are all worth attending to. But there is a separate financial event landing at the start of July that receives considerably less planning attention, despite being entirely predictable in its timing and approximate scale.

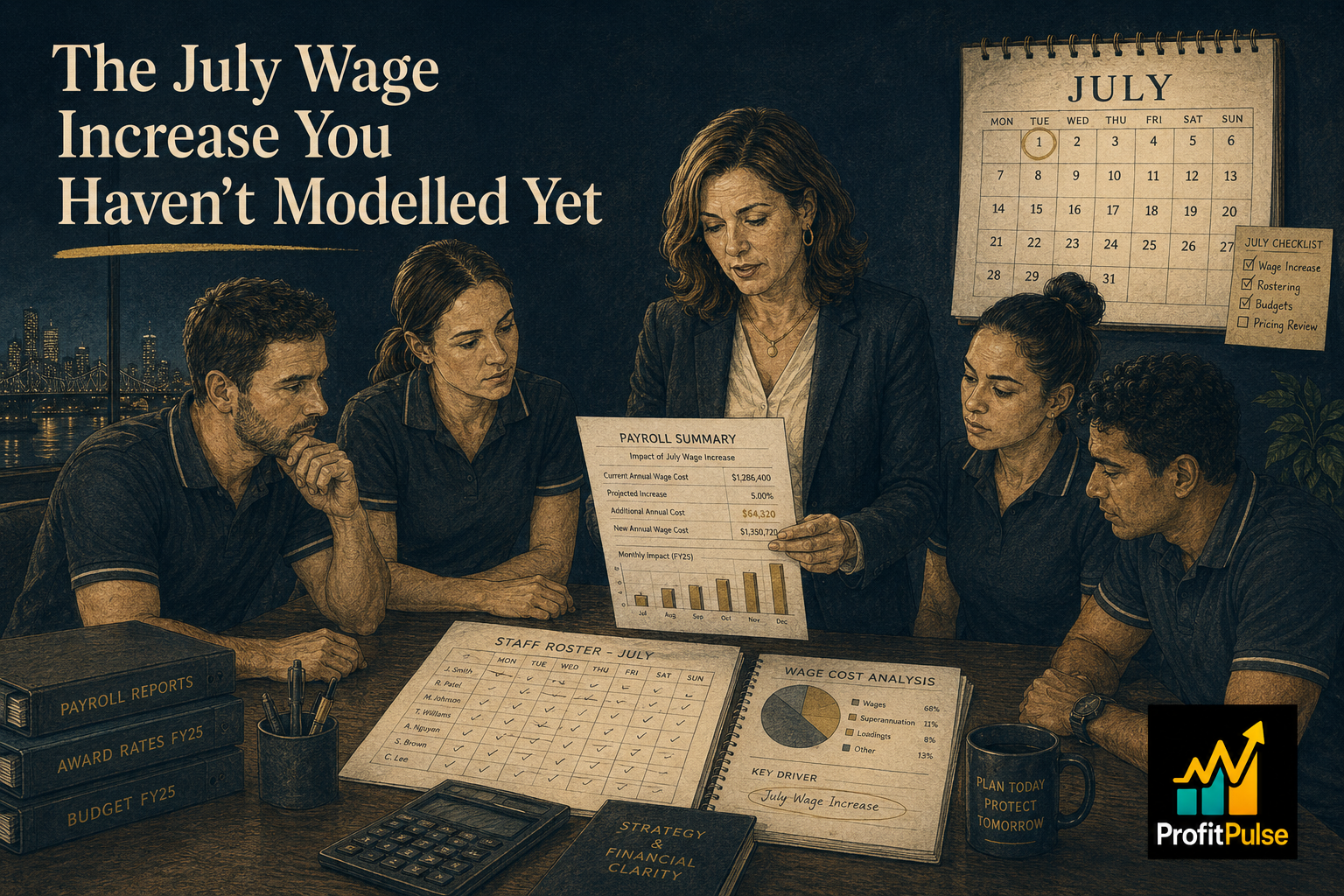

Every June, the Fair Work Commission announces its annual decision on minimum wages and the modern award rates that govern most of Australia’s award-covered workforce. The new rates take effect from the first full pay period on or after 1 July. For businesses with award-covered staff in hospitality, retail, childcare, aged care, construction, and allied health, this is not an abstract policy outcome. It is a direct increase to payroll costs, landing in the first pay run of the new financial year, regardless of how recently the business reviewed its pricing or set its budget.

Most business owners are aware the increase is coming. Fewer have modelled what it actually means for their specific payroll. That gap between awareness and preparation is where the cash pressure typically shows up, not as a surprise, but as a compressed period in early July that was entirely foreseeable and entirely plannable.

The Mechanism Is Straightforward. The Cash Impact Is Not.

The FWC decision applies to every employee on a modern award at or near the minimum classification rates. From the first full pay period after 1 July, the base rate for each covered classification increases. The increase is immediate, applies across all award-covered roles simultaneously, and compounds through several parts of the payroll calculation that most owners do not work through when they read the headline percentage.

Superannuation is calculated as a percentage of ordinary time earnings. When the base wage increases, the employer’s super obligation increases proportionally for every affected employee. The Q1 superannuation contribution for the new financial year does not fall due until late October, but the liability accrues from the first pay period in July and represents a genuine forward obligation that sits in the business’s working capital picture from the start of the new year.

Annual leave loading of 17.5 percent applies under most modern awards when employees take leave. It is calculated on the base ordinary time rate, which means a higher base rate produces a higher leave loading cost for every employee who takes leave in the months that follow. For businesses that see concentrated leave-taking in July and August as teams wind down after EOFY, the effect on payroll outflows in those months is amplified beyond what the ordinary rate movement alone implies.

Penalty rates, casual loadings, and overtime calculations are all derived from the ordinary time rate. A hospitality business running weekend trade, a childcare centre with shift differentials, or a construction firm paying overtime through the June push will see the rate increase flow through every hour worked under a loading, not just standard hours. For businesses with complex rostering across different shift types, the effective increase in total wage cost is consistently larger than the base rate percentage implies when applied to ordinary hours alone.

Building It Into July Planning Before the First Payroll Runs

The FWC announcement in June gives businesses a working window to calculate the real impact before it arrives. The useful exercise is arithmetic: take the actual roster for an ordinary week, apply the new award classification rates to each role and shift type, and compare the total to the current weekly payroll figure. The difference is the real cost increase per pay period, and it is almost always higher than the estimate most owners carry in their heads after reading the announcement.

For a business with fifteen award-covered employees across a mix of full-time, part-time, and casual roles with weekend penalties, this calculation regularly produces a figure that is noticeably larger than the headline rate implies. Understanding the precise number before 1 July means it can be incorporated into a cash flow view for the new financial year’s opening weeks, rather than appearing as an unexplained tightening in the first payroll reconciliation of the year.

A 13-week cash flow forecast updated with the new payroll costs before 1 July shows the specific weeks where the cash position tightens. For most businesses, July and August carry the most concentrated pressure: new financial year revenue is still building from its post-EOFY transition, the superannuation guarantee for Q4 FY26 falls due on 28 July for businesses that have not pre-paid, and the higher payroll costs are running from the first week of the new year.

The second question worth addressing before the year turns is pricing. For businesses that have not reviewed their fee schedules or prices since late 2025, the July increase arrives on top of any previous years’ award increases that were not fully recovered in the rates charged to customers. The compounding effect of two or three years of unrecovered wage cost growth is one of the more consistent explanations for why gross margin drifts lower in labour-intensive businesses without any single, identifiable turning point. A pricing review completed before the new financial year begins captures this year’s cost increase in the schedule before another twelve months of margin erosion can accumulate.

ProfitPulse works with owner-led businesses across Queensland and NSW to build the forward cash picture that turns predictable cost events into planned-for items rather than July surprises. If the new payroll rates have not yet been modelled into your cash position for the first quarter of FY27, that arithmetic is worth completing before the first pay run of the year arrives. Book a complimentary 45-minute discovery call with ProfitPulse.

Frequently asked questions

When does the Fair Work Commission annual wage increase take effect in Australia?

The Fair Work Commission typically announces its annual wage decision in June, and the new rates take effect from the first full pay period on or after 1 July each year. Most businesses see the increase flow into payroll in their first or second pay run of the new financial year, with no transitional period. Businesses that discover the new rates late are absorbing the cost from day one without having planned for it, which is what makes the June window for preparation worth using.

Which industries are most affected by annual award wage increases in Australia?

Hospitality, retail, childcare, aged care, allied health, construction, cleaning services, and transport tend to be most exposed because a significant share of their workforce is covered by modern awards at or near minimum classification rates. Businesses in these sectors also commonly carry casual employees and weekend or evening rosters, which amplify the increase through penalty rates and casual loadings. The headline rate understates the total payroll impact for most businesses in these clusters once loadings are applied.

How do I calculate the full payroll cost of a wage rate increase for my business?

Start with your actual roster hours broken down by employee type and award classification. Apply the new rates to each role, including casual loadings, penalty rates for weekend or evening hours, and any overtime. Compare the total to your current weekly payroll and multiply by your pay frequency. This figure is almost always higher than multiplying the headline rate percentage by total wages, because loadings and penalties compound the base rate change across every hour worked under those conditions.

Does my superannuation obligation also increase when award wages go up in Australia?

Yes. Superannuation is calculated as a percentage of ordinary time earnings, so when the base award rate increases, the employer’s super obligation increases proportionally for every affected employee. The Q1 contribution for the new financial year does not fall due until October, but the liability accrues from the first July pay period and reduces the working capital available in the meantime. A forward cash flow model built in June captures this accrual in the opening quarter’s picture before it arrives.

Can I raise my prices to recover the July award wage increase in Australia?

This is worth examining before the new financial year begins, not after. If prices have not been reviewed since last July, the new increase arrives on top of any previous years’ award increases not yet recovered in your fee schedule. The compounding of two or three unrecovered increases is a common explanation for why margin drifts lower in labour-intensive businesses without an obvious cause. A pricing review in June recovers the cost before another year of silent erosion can accumulate through FY27.

How does a fractional CFO help a business manage annual wage cost planning?

By building and maintaining the payroll cost analysis and forward cash modelling that lets a business respond to annual wage decisions before they arrive rather than after. For businesses with complex award coverage across multiple classifications and shift types, a fractional CFO arrangement includes the full payroll impact calculation, a cash flow update for the first quarter of the new financial year, and a recommendation on whether the cost increase warrants a pricing review before July.

What is the difference between the national minimum wage and a modern award rate in Australia?

The national minimum wage is the floor rate for employees not covered by a modern award or enterprise agreement. Modern award rates sit above that floor for most classifications and are reviewed by the Fair Work Commission each year. Most employees in industries such as hospitality, retail, healthcare, and construction are covered by a modern award, which means the relevant award classification rate for their role determines their minimum pay, not the national minimum wage figure announced alongside it.

Leave a Reply