Every year, as June approaches, the same pattern plays out across owner-led businesses on the East Coast. Equipment suppliers run EOFY campaigns. Technology vendors extend payment terms. Advisers field calls about what to buy, prepay, or write off before June 30. The underlying instinct is reasonable: the financial year is closing, benefits from asset purchases and prepaid expenses are real, and tidying up the books before year end makes commercial sense.

What gets skipped, more often than it should, is a straightforward calculation: when does the cash leave, and when does the benefit arrive?

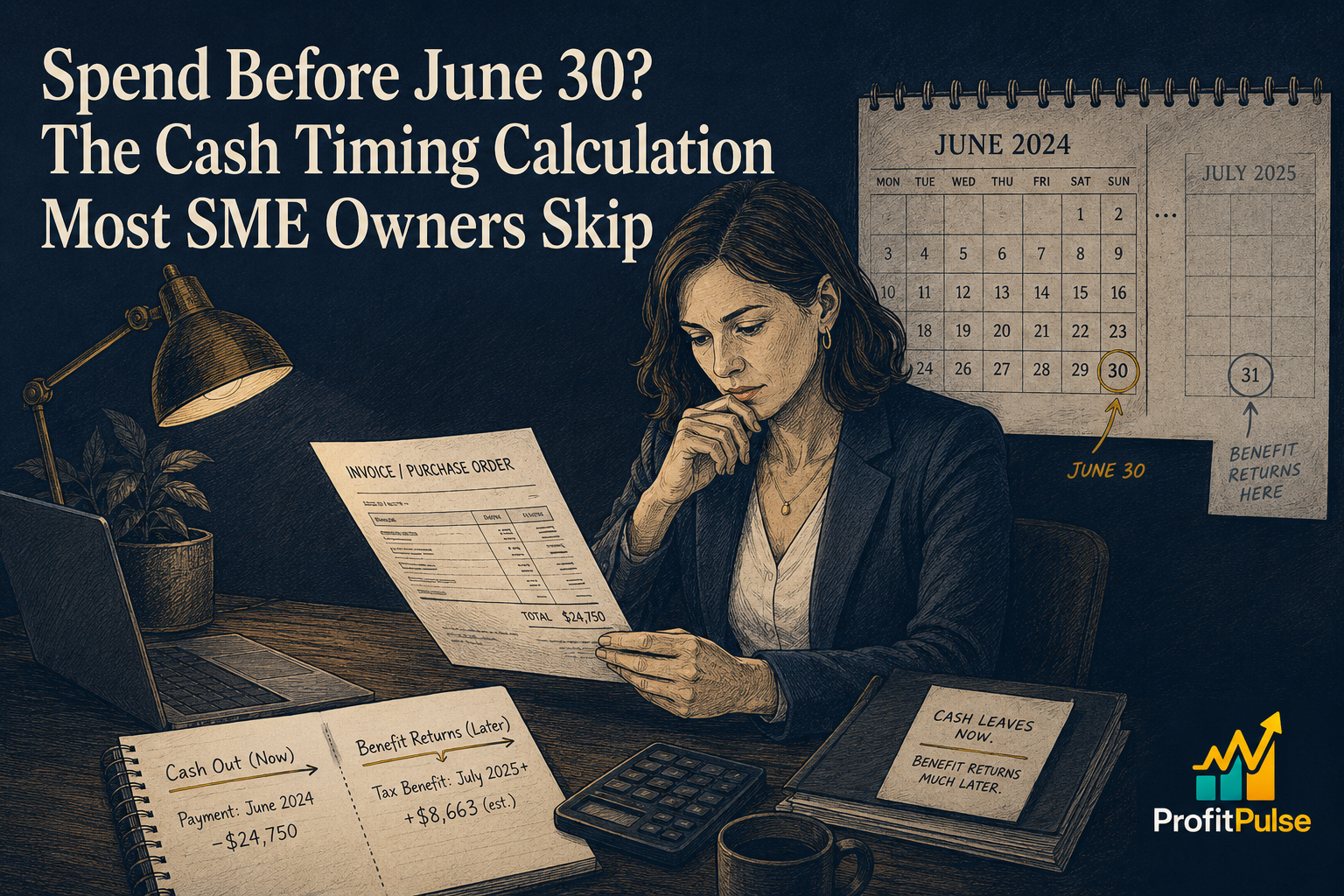

For most EOFY purchase decisions, the cash leaves the account in June. The tax position is resolved considerably later. The business carries the gap, and that gap tends to show up most painfully in July and August, when the new financial year is still warming up and prior-year revenue has already been spent.

The Timing Gap That Catches Businesses Out

When a business settles a significant invoice before June 30, whether for equipment, technology, prepaid services, or additional stock, the cash effect is immediate. The bank account falls on the day the funds transfer. That is the whole story from a cash perspective.

The tax position is different. For most Australian businesses, the benefit from an EOFY purchase flows through the income tax return for the year ending June 30. That return is typically lodged somewhere between August and May of the following year, depending on whether the business uses a tax agent and which lodgement group it falls into. The resulting reduction in tax payable arrives later still.

This means the business funds the full cost of the purchase from its own cash reserves from June onward, through the months where the new financial year’s revenue is still building and the prior year’s collections are running down. The benefit is real, but it is not immediate, and the difference between understanding that timing and not understanding it can be the difference between a comfortable new year and a pressured one.

For a purchase of $40,000, the cash outflow in June is $40,000. The eventual tax reduction is a fraction of that, determined by the business’s applicable rate, and it arrives months after the purchase was made. A business that plans its June commitments with that timing in mind makes a different decision than one that treats the tax saving as arriving at the same moment as the cash leaves.

The Three Categories Worth Slowing Down On

Not every EOFY purchase is a trap. An asset the business genuinely needs, with clear expected returns and cash that comfortably supports the outlay, is a sound decision regardless of the month. What deserves extra scrutiny are the purchases that were not on any priority list in March but became urgent as June approached.

Equipment and technology that was a lower priority in April tends to get reclassified as essential in May. The EOFY deadline creates a kind of artificial urgency that is worth pressure-testing honestly. If an asset genuinely improves revenue or reduces cost, the case holds on its own merits throughout the year. If the main argument for the timing is the tax position, the cash calculation deserves more attention than it usually gets.

Stock and inventory builds fall into the same category. Purchasing ahead of genuine customer demand ties cash up in physical goods while depleting working capital, and inventory carrying costs often erode the benefit when the holding period extends beyond what was expected at the time of purchase.

Prepaid expenses can be useful for EOFY planning in the right circumstances, but they carry the same basic question: is this commitment something the business would make regardless of the date, or is the financial year end doing most of the work?

What a Clear Cash View Changes

The useful discipline here is not to avoid EOFY commitments but to make them from a clear view of the cash position they create, not just for June, but for the two months that follow.

A 13-week cash flow forecast built through June 30 and projected into September shows the actual runway after a purchase, including the standard pressure points that arrive in July: the superannuation guarantee for the April to June quarter is due by 28 July, team entitlements accumulate through the last quarter, and revenue from the new financial year typically lags the calendar by several weeks. Seeing this picture before a purchase decision makes the risk visible rather than abstract.

The questions are simple enough to answer in a short session with the right forward view. What is the cash position in the second week of July after this commitment? What does August look like with that reduction in working capital? Is there a facility, a receivables pipeline, or collections certainty to support the gap if it opens wider than expected?

Owners who work through these questions before June 30 often make the same purchase, but with better timing, staged payment terms, or external financing that spreads the cash impact rather than concentrating it in the month that already carries the most competing obligations. Owners who skip the calculation frequently spend the first two months of the new financial year tightening expenses and chasing debtors to compensate for a cash position that looked fine in June and felt different by August.

ProfitPulse works with owner-led businesses through exactly this part of the calendar, building the forward cash view that turns an EOFY spending decision from a potentially stressful commitment into one the business has genuinely planned for. If the next four weeks involve significant commitments and you do not yet have a clear picture of your July and August cash position, that picture is worth building now. Book a complimentary 45-minute discovery call with ProfitPulse.

Frequently asked questions

How does making a major business purchase before June 30 affect my cash flow?

When you purchase an asset or prepay expenses before June 30, the full cash amount leaves immediately. The tax benefit, a reduction in your income tax for the year, arrives when your return is lodged and processed, typically months later. The business carries the full cash cost through July and August before that benefit materialises, which means the cash position in the new financial year is lower than the year-end bank balance suggested it would be.

When does the tax benefit from an EOFY asset purchase actually arrive for a small business?

For most Australian small businesses using a tax agent, the income tax return for the year ending June 30 is lodged between October and May of the following year, depending on the lodgement group. The tax saving from an EOFY asset purchase therefore reduces a liability or generates a refund many months after the cash was spent. This timing gap is often the difference between an EOFY decision that works commercially and one that creates unnecessary cash pressure in July and August.

What should I check before making a large purchase before the financial year ends?

Three questions matter most. Does the business genuinely need this asset, or is the EOFY deadline the primary driver of the timing? What is the cash position in July and August after the purchase, accounting for superannuation contributions due by 28 July and any revenue lag at the start of the new financial year? Is there a facility or confirmed receivables pipeline to support the gap if cash runs tighter than expected? A forward cash flow model answers all three before the commitment is made.

Why is July often the toughest month for small business cash flow in Australia?

July combines several pressures that fall at the same time. Superannuation for the April to June quarter is due by 28 July. Revenue from new financial year activity is typically still building. Prior-year collections have often already been received. And any significant EOFY purchases made in June have reduced the opening working capital balance. Each pressure is manageable individually; together, they can make July feel harder than the revenue level suggests it should.

What is the difference between a tax deduction and actual cash savings for my business?

A tax deduction reduces your taxable income, which in turn reduces the tax payable on that income. The actual cash saving is a fraction of the deduction amount, determined by your applicable tax rate, and it arrives when the tax return is settled rather than when the purchase is made. A business that spends $50,000 on an asset has a net cash cost for the full period between the purchase date and the date the tax position is resolved, which in most cases spans several months of the new financial year.

How do I forecast my cash position through EOFY and into the new financial year?

A rolling 13-week cash flow forecast built from your accounting data, updated weekly, gives you the forward visibility to plan June commitments with July and August clearly in view. The key inputs are confirmed receivables, committed outflows including superannuation and any planned purchases, and a realistic estimate of new financial year revenue timing. ProfitPulse builds and runs these models for Queensland and NSW businesses through the EOFY period.

Does a fractional CFO help with EOFY cash flow planning for Australian SMEs?

For business owners managing significant EOFY spending decisions alongside the operational demands of a busy June, a fractional CFO arrangement brings the cash modelling and planning support that prevents decisions being made on incomplete information. The most common outcome is that planned purchases either proceed on better timing, with staged payments or a facility in place, or are correctly deferred until the business’s July position is clearer.

Leave a Reply