The moment a serious buyer asks for financial records, customer contracts, staff arrangements, and supplier agreements is the wrong moment to start organising them. By that point, the buyer’s team is working from a structured checklist and the seller is running an urgent filing exercise on a timeline set by someone else’s interest. The gap between those two positions shapes the outcome before a word of negotiation is spoken.

This is the pattern in most business sale processes, and it consistently costs sellers more than they realise. Not through a single dramatic reversal. The value loss in due diligence tends to accumulate through price adjustments, conditional clauses, extended timelines, and in some cases a buyer withdrawal that leaves the seller starting the process again from the beginning.

For businesses that have done the preparation work before any buyer conversation begins, the experience looks different. The information is ready, the story is coherent, and the questions that would otherwise pause the process get answered before they are asked. The negotiating position is genuinely different when the seller controls the information flow rather than reacting to it.

What Buyer Due Diligence Actually Examines

A buyer commencing due diligence is asking one underlying question in many different forms: does this business generate the earnings being claimed, and will those earnings hold after the ownership changes? The answer to that question, and its effect on business valuation, depends partly on how completely the seller has documented it.

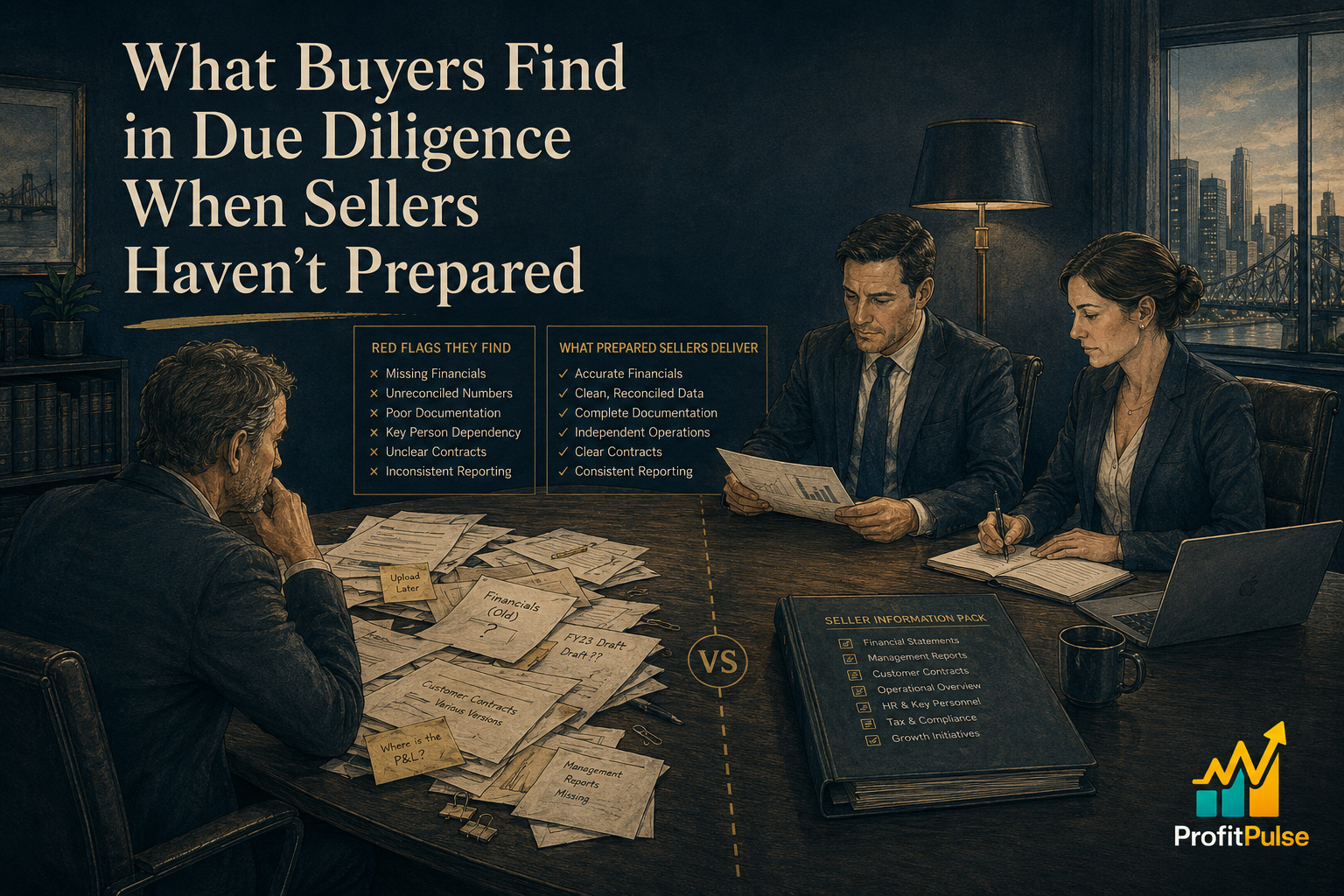

The financial records are the starting point, and the first thing a buyer’s accountant looks for is consistency. Three years of profit and loss statements where cost categories shift between years, where one-off items appear without explanation, or where owner drawings are intertwined with salary in a way that makes maintainable profit hard to determine, will generate a sustained series of clarifying questions. Each question answered introduces another. The process slows. The buyer’s confidence in the headline number declines.

Customer data receives similar scrutiny. A business that claims revenue from a stable, diversified customer base needs to demonstrate it in the data. If the top five customers account for sixty percent of revenue and no formal contracts are in place, the buyer prices that concentration risk directly into the offer. Supplier arrangements, employment contracts, leases, and any ongoing regulatory matters all feature in a complete due diligence process. Each item the buyer’s team has to chase down individually takes longer than one that was pre-prepared, and time pressure in any deal tends to run against the seller.

How the Scramble Changes What the Seller Receives

When sellers are unprepared for due diligence, the most common outcomes are not dramatic failures. They are quieter erosions. A price adjustment in exchange for an undocumented add-back. An earnout clause added to cover the buyer’s uncertainty about whether client relationships will survive the ownership change. A delayed settlement while missing records are reconstructed.

Each of these represents value the seller did not collect, and these adjustments typically happen when the seller is most committed to completing the transaction, months in, with professional fees already spent and alternative buyers no longer being actively managed. The leverage has shifted. Accepting a compromise at that point is easier than it would have been at the outset, and buyers know this.

The businesses that avoid this pattern have prepared the information before the process began. The vendor due diligence work is complete. Questions arrive with answers already ready. The deal process moves faster, and faster processes are less susceptible to the erosion that accumulates when uncertainty is prolonged.

What a Seller-Prepared Information Pack Changes

A vendor due diligence pack is a structured, pre-prepared collection of the financial and commercial information a buyer’s team would request in a standard due diligence process, assembled and reviewed before the business goes to market. It contains the normalised financial history with documented add-back adjustments, a customer revenue and retention analysis, a summary of key contracts and their transferability, employment structure and key staff details, and an operational overview showing how the business functions without the owner day to day.

The practical effect of arriving at a sale process with this material ready is considerable. The buyer’s due diligence period is shorter because fewer requests generate follow-up rounds. The seller’s narrative is established before the buyer’s interpretation of events can take hold. And the quality of the information pack itself signals something to the buyer: that the business is well-run, that its records hold up under scrutiny, and that the financial story being told reflects what an independent party actually found.

A Vendor Due Diligence Pack built from EOFY accounts, when twelve months of complete data are available, is most effective when prepared a full year or more before a planned transaction. An Exit Readiness Diagnostic completed alongside it scores the business across the eight dimensions buyers examine most closely and identifies which gaps in the information pack would create the most exposure in a negotiation.

ProfitPulse works with business owners across Queensland and NSW at this stage of the preparation process, building the financial clarity and documentation quality that changes both the valuation a business attracts and the probability that the deal completes on the seller’s terms. If a sale is under consideration in the next two to three years and the due diligence documentation has not yet been assembled, building that foundation now, with the full financial year’s data fresh and available, is the most productive use of the current period. Book a discovery call with ProfitPulse.

Frequently asked questions

What is vendor due diligence and how does it differ from buyer due diligence?

Vendor due diligence is a review the seller commissions of their own business before any sale process begins, producing a pre-verified information pack that sets the frame for subsequent buyer conversations. Buyer due diligence is the independent review a buyer conducts of the target business during a transaction. The key difference is timing and control: vendor due diligence allows the seller to address gaps before they become objections under deal pressure, and typically produces a shorter process and fewer price adjustments than a reactive approach.

What documents does a buyer typically request during business sale due diligence in Australia?

Buyers commonly request three years of financial statements, a current debtors and creditors ledger, key customer contracts and revenue history by client, supplier agreements and terms, employment contracts including any non-standard arrangements, lease documentation, details of any regulatory matters or disputes, and a clear explanation of the normalised earnings figure used for valuation. Each item the seller cannot produce promptly extends the process and generates additional rounds of follow-up questions.

How does the due diligence process affect the final sale price of a business?

Due diligence creates conditions for price adjustment in either direction. Sellers who arrive with clean, pre-prepared documentation and clearly auditable earnings maintain the valuation they were seeking. Sellers whose records require reconstruction or whose earnings need documentation under deal pressure typically accept adjustments to secure the transaction. The most common outcomes for unprepared sellers are price chips for undocumented add-backs, earnout clauses for uncertain client transfer, and delayed settlement while missing records are assembled.

What should I include in a vendor due diligence pack when selling my Australian business?

A vendor due diligence pack typically includes a three-year normalised financial history with documented add-backs reconciling to the accounts, a customer revenue and retention analysis by client, a summary of key contracts and their transferability, employment and staff details, and an operational overview showing how the business functions without the owner. Building it from EOFY data, when the full year is available, gives the pack its most complete and auditable foundation. An exit readiness guide covers the preparation in more detail.

How far in advance should I start preparing for business sale due diligence?

Starting twelve to twenty-four months before a planned sale gives adequate time to address any financial record gaps, document normalisation adjustments properly, and allow structural improvements to appear in two or more years of accounts before a buyer reviews them. An Exit Readiness Diagnostic at this stage identifies which preparation steps will have the most impact on the sale outcome and sequences them so the highest-value work happens first.

What is an earnout clause in a business sale and how do sellers avoid them?

An earnout is a deferred payment structure where part of the sale price depends on the business meeting agreed targets after the ownership transition. Buyers propose earnouts when they are uncertain whether the business’s earnings will hold after the owner departs, or whether key client relationships will transfer. Sellers who have documented their customer relationships, demonstrated management team depth, and provided a clean auditable financial history are less likely to face earnout requirements, because the uncertainty driving the clause has been reduced by the preparation work.

How does a fractional CFO help a Queensland business owner prepare for sale due diligence?

For business owners managing daily operations while preparing for a sale, the financial documentation work required for credible due diligence is genuinely time-consuming. A fractional CFO arrangement builds the normalised earnings history, ensures financial records are clean and auditable across the preparation period, and coordinates the vendor information pack so it is ready before any buyer approaches. The investment is typically recovered through a better negotiated outcome in the sale itself.

Leave a Reply