World Environment Day falls on 5 June, and for solar, battery, and EV charging installation businesses across Queensland, NSW, and Victoria, the timing carries genuine commercial weight. June is consistently the highest-volume sales month in the residential solar calendar, driven by Small-scale Technology Certificate deadline incentives and the broader EOFY consumer spending period. Installation teams are committed weeks out. Quote volumes are at their peak. By the end of the month, most solar installation businesses will record their strongest revenue figure of the year.

What rarely receives the same attention is what that surge does to working capital, unit economics, and cash timing. The installation pipeline building through May and June creates a specific financial pattern, one that repeats annually and one that most businesses manage reactively rather than by design.

The good news is that planning for it is straightforward once the mechanism is understood.

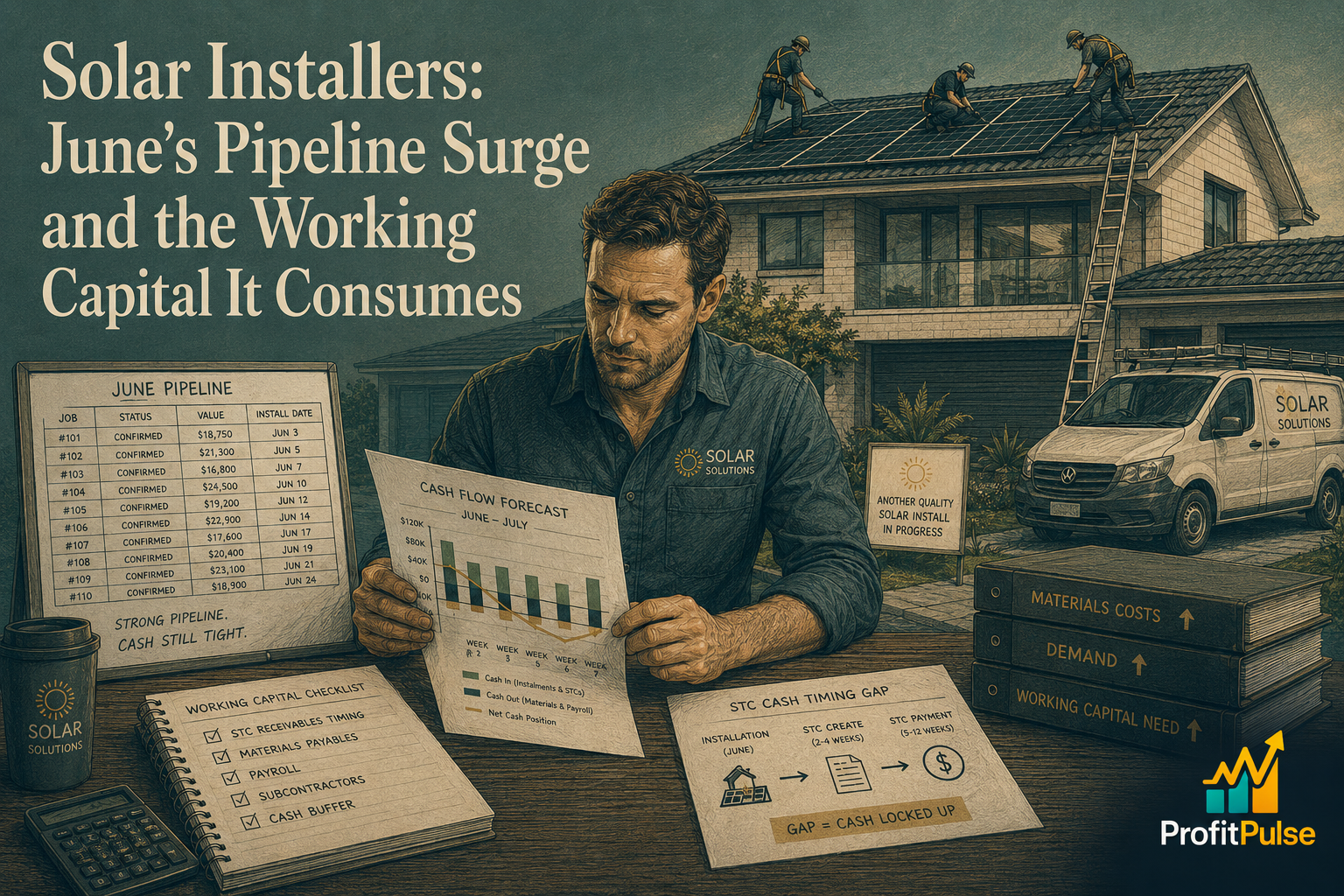

How the Small-scale Technology Certificates (“STC”) Mechanism Creates a Cash Timing Mismatch

STC’s are the federal rebate mechanism that reduces the upfront cost of residential solar and battery installations for consumers. An accredited installer who assigns STCs on the customer’s behalf receives the corresponding payment from a registered agent, typically at a rate reflecting the current STC spot price.

The timing of that payment matters. STC assignment can take several days to two weeks to process, depending on the agent and the validation cycle. An installer completing high volumes of jobs in June may find a meaningful portion of STC receipts landing in July, after the financial year has closed and while the new year’s pipeline is still building. The job is billed. The revenue is recognised. The cash arrives on a different calendar.

This timing gap is not unique to solar. What makes it significant for installation businesses is the compounding effect of volume. When a large number of jobs complete within the same four to six-week window, the STC timing gap across the full batch concentrates the cash shortfall into the same period, usually mid-July to August. Combined with superannuation contributions due by 28 July (last occurrence in the current regulations) for the April to June quarter, the cash position in early July can feel considerably tighter than the June revenue figures suggest it should.

The Real Unit Economics of an Installation Job

Most solar installation businesses track revenue per job and total jobs per month. Fewer consistently run a unit economics calculation that applies all direct costs to each job category and produces a genuine contribution margin figure.

Direct costs on a residential solar installation include panels and inverter, battery if applicable, mounting hardware and cabling, installation labour, electrical compliance certification, and any site-specific access requirements. Where a subcontractor completes the installation rather than an employed team, the subcontract rate absorbs a share of margin that varies materially by job type and by subcontractor availability in the current market.

Material costs for panels and inverters have moved considerably over recent years. An installer whose margin assumptions were built on earlier procurement pricing may be pricing jobs today against those older calculations while paying current materials costs. The contribution margin per job is lower than the historical model implies. The total revenue figure looks strong. The bank account at month end tells a quieter story.

A review of costs and margins across job types, residential, commercial rooftop, battery-only additions, and EV charging, surfaces which categories are genuinely profitable at current costs and which have drifted. For most installation businesses, at least one category will be priced below its real cost of delivery. A Cost and Margin Deep Dive across the business’s job structure produces a ranked view of which work to protect, reprice, or move away from, using the twelve months of job data that EOFY makes available.

What EOFY Means for an Installer Thinking About Growth or Exit

The weeks after June 30, when a full year of job and financial data are available, are the natural moment for a solar installation business to review its medium-term financial direction.

For businesses planning growth, the cash timing analysis above determines whether existing working capital facilities support the scaled order book or whether a facility review is warranted before the pipeline grows further. A working capital review at this point maps where cash is committed across the pipeline, identifies the specific timing gaps between materials outlay, installation completion, and STC receipt, and produces a prioritised action list to improve the position before it creates avoidable pressure.

For business owners thinking about an eventual sale, whether that is two years away or five, the EOFY financials are the foundation from which a valuation is built. Solar installation businesses that are owner-operated, with the principal personally holding key subcontractor relationships and handling commercial quoting, tend to attract lower multiples than businesses where these functions sit within the team. An Exit Readiness Diagnostic at this point scores the business across the eight buyer-grade readiness dimensions and identifies which structural changes would most meaningfully improve the valuation outcome in the years before a planned transition.

June’s pipeline surge is commercially valuable. Converting that performance into decisions that serve the year ahead and the business’s longer-term financial direction is where the real work sits. ProfitPulse works with trade and installation businesses across Queensland and NSW at this point in the calendar. If June has delivered strong numbers and the July working capital position is not yet clearly mapped, that picture is worth building now. Book a complimentary 45-minute discovery call with ProfitPulse.

Frequently asked questions

Why does my solar installation business have strong revenue but tight cash flow in July?

The timing gap between completing installations, assigning Small-scale Technology Certificates, and receiving payment from STC agents typically runs one to three weeks. When a large volume of June jobs complete in the same window, the combined STC receipts land in mid-July while wage costs, superannuation obligations due by 28 July, and materials invoices fall in the same period. The revenue is real. The cash arrives later, and planning for that timing prevents a predictable situation from becoming a surprise each year.

How are Small-scale Technology Certificates treated in a solar business profit and loss?

STCs assigned on behalf of customers and paid to the installer are recognised as revenue when the right to receive payment is established, typically at installation completion. The STC spot price at the time of assignment determines the value. Where STC income is material to total revenue, separating it from installation and labour revenue in the management accounts clarifies the true margin contribution of each component and how each moves as market conditions change.

What gross margin should a residential solar installation business be making per job?

Contribution margins vary considerably by job type, labour structure, and subcontract versus employee model. Residential solar jobs with a direct labour team typically target gross margins in the 25 to 40 percent range before overhead allocation. Jobs subcontracted entirely sit lower. Battery-only additions and commercial rooftop jobs often carry different margin profiles from residential volume work. Running a job-level cost analysis across each category surfaces which types are actually contributing and which have been priced below their real current cost.

How do I improve working capital for my solar and battery installation business?

The most effective actions are managing STC assignment timing to reduce the gap between job completion and receipt, tightening upfront deposit structures on larger jobs to fund materials before labour costs fall, and negotiating supplier payment terms on panels and inverters that align with the typical installation-to-collection cycle. A Working Capital Unlock maps these timing gaps specifically for installation businesses and produces a prioritised action list to release cash trapped in the cycle.

What is a typical valuation multiple for a solar installation business in Australia?

Multiples generally range from two to four times normalised annual profit for owner-operated businesses and four to six or more for businesses with a capable management layer, some recurring maintenance or monitoring revenue, and subcontractor relationships that are not personally held by the owner. The quality of financial records, documented installation systems, and the absence of customer concentration in commercial work typically determine where in the range a particular business sits. Business valuations for Queensland SMEs covers installation businesses as part of the trades and services sector.

What financial metrics matter most for growing a solar installation business in Australia?

Revenue per installed kilowatt, contribution margin per job category, STC income as a percentage of total revenue, subcontract labour ratio, and cash conversion cycle from installation completion to receipt. Together these tell you whether the business is generating durable margin or volume that looks profitable on the P&L but is not. Most installation businesses already hold this data in their job management system; the question is whether it is being used to make pricing and capacity decisions.

When should a solar installer start preparing the business for sale or succession?

Starting three to five years before an intended exit gives the business time to address owner dependence, build any recurring revenue component, and present a clean multi-year financial history that buyers can read with confidence. An Exit Readiness Diagnostic done at EOFY, when twelve months of complete data are available, establishes the baseline and identifies which of the eight buyer-grade readiness dimensions needs the most focused attention in the years that follow.

Leave a Reply