By the time June 30 arrives, most owner-led businesses have one number on their minds: profit. What did the year deliver? Is the P&L where it needs to be for the tax return? For owners thinking further ahead, a second question follows: what does this year’s result say to a future buyer?

But there is a third reader of your June 30 accounts, and it draws its own conclusions without waiting to be asked. Your bank and the lenders behind any existing facility automatically reassess the quality of their exposure when annual financials are lodged and ratios recalculated. The number they care about most is not your net profit. It is the structure of your balance sheet, and specifically whether your assets and liabilities still support the facilities you hold. For a business with an overdraft, a trade finance line, or equipment debt, this reassessment directly determines whether that facility renews without friction, stays flat, or prompts a conversation you did not expect.

Understanding what your lender reads, and which decisions remain available before June 30, is a separate exercise from the compliance work your bookkeeper and accountant carry out at year end. Both are necessary. They answer different questions for different audiences.

What the Balance Sheet Shows That the P&L Cannot

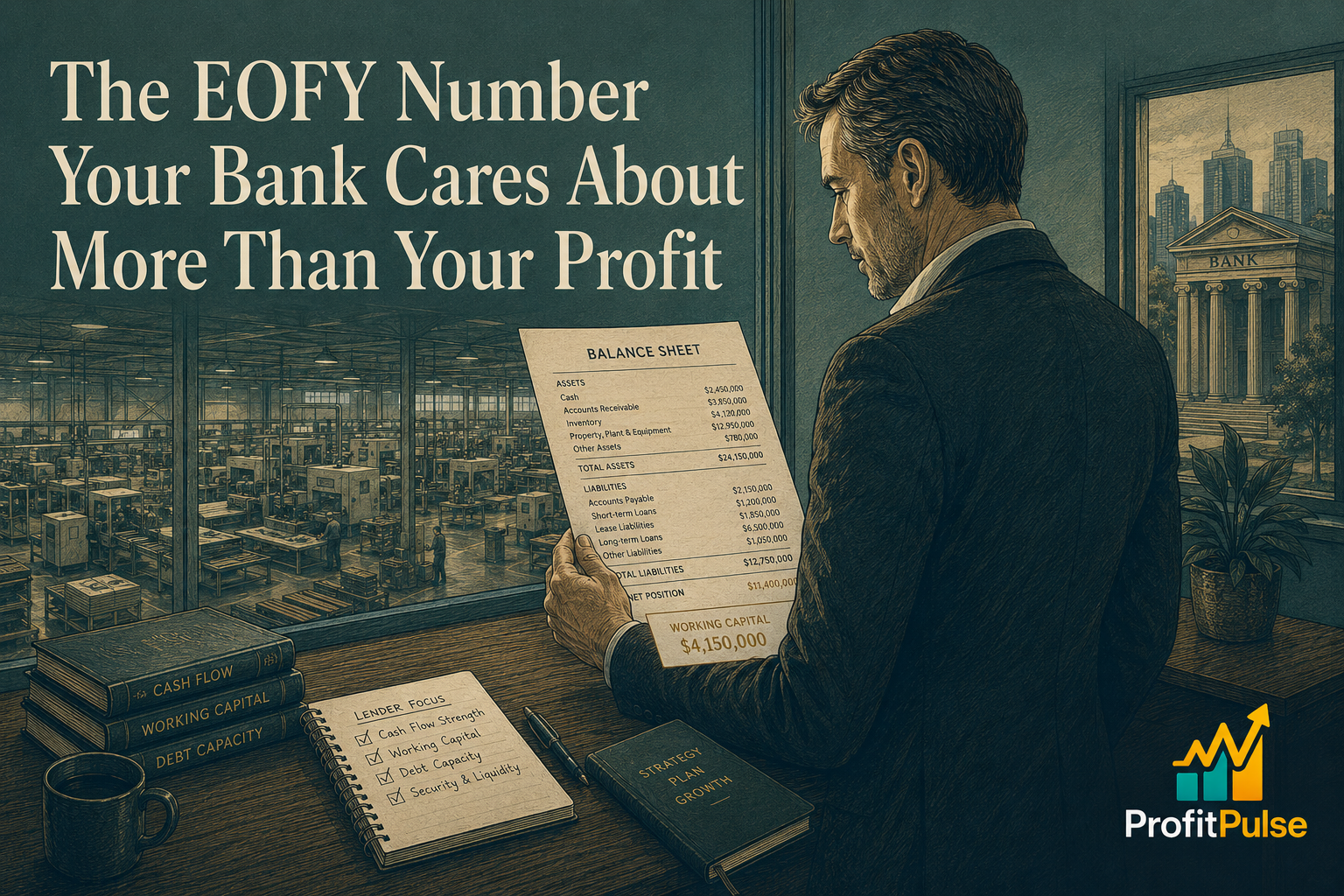

The profit and loss statement is designed to report taxable income. Lenders are considerably less interested in that figure than most business owners assume. They focus on the balance sheet and the cash flow statement because those describe the business’s structural capacity to service and repay debt, which is the question that actually matters when a facility is on the table.

The metric that appears most consistently in commercial lending assessments is the current ratio: current assets divided by current liabilities. A ratio below 1.0 means short-term obligations exceed short-term resources, signalling that the business relies on forward revenue or external credit to remain liquid. Most commercial lenders require a current ratio of at least 1.2 before extending or renewing a working capital facility.

Debtor quality matters as much as the receivables balance. A ledger with significant amounts aged beyond 60 days tells a lender that revenue is not converting to cash at the pace the P&L implies. A business with $800,000 in receivables, of which $300,000 sits past 60 days, presents a different risk profile than one with the same total and a current ageing profile. The quality, not just the quantity, is what drives the lender’s assessment of your working capital cycle.

Debt service coverage ratio, which compares annual earnings to the total annual cost of servicing all debt, tells the lender whether the profitability of the business is sufficient to carry its existing load. In a period where rates have risen materially, this ratio has tightened for some businesses even when profit has held steady, because the denominator has grown. A covenant that was comfortable two years ago deserves a fresh check today.

The June 30 Decisions Still Available

Several practical steps can improve the balance sheet picture before the financial year closes, and none of them require a structural change to the business.

Collecting aged debtors is the most immediate lever. Every dollar collected before June 30 converts a receivable to cash, improving both the current ratio and the ageing profile a lender reads. A focused two-week collection effort in the second half of June, starting with balances beyond 60 days, can shift the picture materially. For businesses where the debtors ledger has become a persistent issue, a Debtor and Collections Reset compresses this work into a structured sprint with templates, a dunning workflow, and clear accountability.

Avoiding unnecessary draws on revolving credit facilities in the final days of June is worth attention. A bank that sees the overdraft at its ceiling on the June 30 statement reads a more constrained business than one with visible headroom. Where a draw can be deferred by a few days into the new financial year without operational consequence, the year-end position reflects the business on a normal day rather than at a moment of peak pressure.

Reducing short-term liabilities where practical also improves the current ratio before the snapshot is taken. Settling supplier invoices that fall due in the final days of June, where cash supports it, removes near-term obligations from the balance sheet and ensures June 30 captures the genuine operating position rather than a momentary tightness the following week would have resolved on its own.

The Banking Conversation Worth Having After June 30

With clean EOFY financials available, the weeks after June 30 are the most productive moment for a business to revisit its banking arrangements. For most Australian SMEs, this conversation has not happened recently enough. The overdraft was sized when the business was smaller. The pricing has not been reviewed since the original application. The security structure may not reflect a business that has grown considerably since the facility was first negotiated.

An independent Banking and Facility Review at this point assesses whether existing facilities are structured correctly for the current business, whether pricing reflects the present credit profile, and whether the June 30 financials support a case for better terms or increased headroom. Many businesses find that savings on interest and fees within the first year cover the cost of the review outright.

For businesses planning growth, an acquisition, or a material capital investment in the year ahead, capital raise preparation done in July and August with fresh EOFY accounts as the foundation produces a sharper picture of what the business can credibly support, from which type of provider, and at what cost of capital.

ProfitPulse works with owner-led businesses across Queensland and NSW at exactly this point in the year. If the banking conversation has not been part of your EOFY planning and your June 30 accounts are taking shape, that picture is worth building before the financial year closes. Book a complimentary 45-minute discovery call with ProfitPulse.

Frequently asked questions

What does my bank actually look at in my business financial statements?

Lenders focus primarily on the balance sheet and the cash flow statement rather than the profit and loss. The key indicators are the current ratio, the ageing profile of your receivables, and your debt service coverage ratio. These tell a lender whether the business can meet its short-term obligations and carry its existing debt load. The P&L tells them whether you made a profit; the balance sheet tells them whether that profit left the business in a financially sound position.

What is a good current ratio for a small business in Australia?

Most commercial lenders look for a current ratio of at least 1.2, meaning current assets are at least 20 percent higher than current liabilities. A ratio below 1.0 signals that the business is relying on forward revenue or external credit to meet near-term obligations, which increases perceived lending risk. For businesses with lumpy or seasonal revenue, a higher ratio is often expected before a facility is extended or renewed, because the buffer needs to absorb a longer period of uneven cash timing.

Can I improve my balance sheet before June 30 to help my borrowing position?

Yes, and the most effective actions are straightforward. Collecting debtors aged beyond 60 days converts receivables to cash, improving your current ratio and your lender’s view of receivables quality. Avoiding unnecessary draws on revolving facilities in the final days of June reduces the liability side of the current ratio. Settling short-term supplier obligations where cash supports it removes near-term liabilities before the year-end snapshot. Each action is modest on its own; the combination can shift the lender’s picture meaningfully.

What is debt service coverage ratio and how does it affect my business loan in Australia?

Debt service coverage ratio, or DSCR, compares annual earnings to the total annual cost of servicing all debt, including principal and interest across every facility. Most commercial lenders require a DSCR above 1.25, meaning earnings need to be at least 25 percent more than total debt repayments. After a period of rising rates, some businesses have moved closer to their covenant threshold even without a fall in profit, because interest costs have grown. Checking this figure before the annual review avoids surprises.

What is a Banking and Facility Review and when should an Australian SME consider one?

A Banking and Facility Review is an independent assessment of whether your existing bank facilities, their pricing, structure, and covenant terms, still fit the business as it is today. Most facilities are established once and rarely revisited, which means many businesses pay pricing that reflects their credit profile from years earlier and hold limits sized to an older version of the business. The post-EOFY period, when fresh financials are available, is the natural moment. ProfitPulse’s Banking and Facility Review is structured to recover its cost through first-year savings.

How does a fractional CFO help with bank relationships and facility negotiations for SMEs?

A fractional CFO brings the financial modelling, covenant monitoring, and lender relationship experience that most business owners lack when dealing with banks. This includes preparing the financial narrative and supporting documentation for a facility review, tracking covenant compliance throughout the year, and identifying when conditions are right to approach a lender for improved terms. For SMEs between three and twenty million in revenue, this is the banking oversight a full-time CFO would provide, at a fraction of the cost.

When is the best time for an Australian SME to renegotiate or review its bank facilities?

The weeks immediately after June 30, when twelve months of clean financials are available, are the strongest position from which to approach a lender. Fresh accounts make the case for improved terms or increased headroom more clearly than interim or draft financials do. If the business has grown, strengthened its balance sheet, or improved its debt service coverage during the year, that improvement is now fully documented and ready to support a conversation about better pricing or facility structure. ProfitPulse supports Brisbane and Queensland businesses through exactly this process.

Leave a Reply