Revenue moves through a business in two stages. The first is when the work is done and the invoice goes out. The second is when the payment lands in the account. For most owner-led businesses, it is the second stage that determines how comfortable or pressured the month feels, regardless of what the first stage delivered.

The gap between those two stages is measurable. It has a name, Days Sales Outstanding, and it is calculated from data every business already holds: the outstanding receivables balance and the revenue generated in the same period. DSO tells you, in plain terms, how many days on average pass between issuing an invoice and receiving the cash.

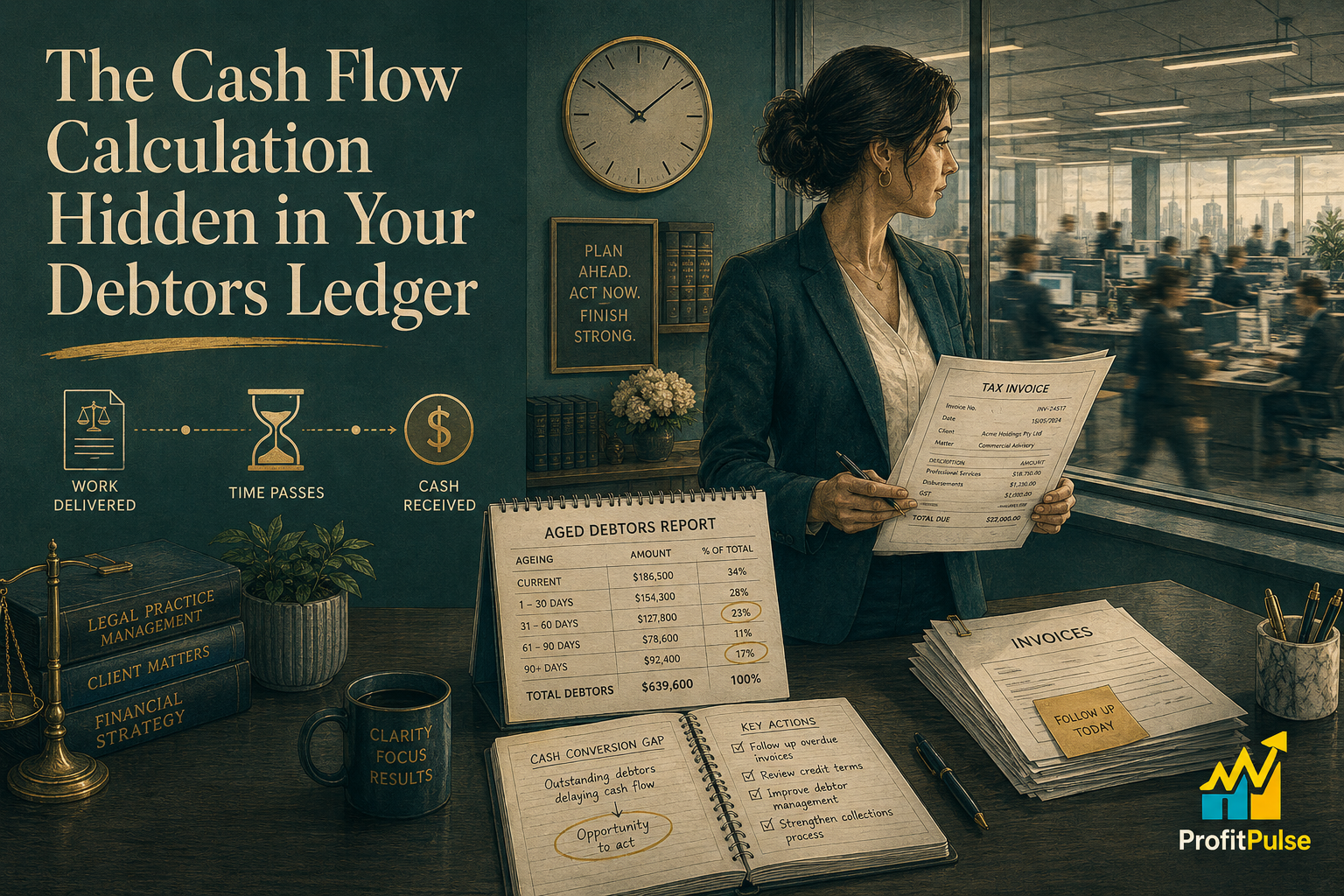

With June 30 two weeks away, the receivables balance at the end of the financial year becomes the opening working capital position for FY27. Understanding how that balance is built, and what reducing some of it before year end would mean for the July cash position, is a calculation worth doing before the month closes.

What the DSO Calculation Actually Shows

A straightforward way to calculate DSO is to take the current accounts receivable balance, divide it by average monthly revenue, and multiply by 30. For a business generating $4 million annually, that is roughly $333,000 in monthly revenue. If the receivables balance sits at $500,000, the Days Sales Outstanding (DSO) is approximately 45 days. The average invoice is taking 45 days to convert to cash.

The comparison that makes that number meaningful is the business’s own payment terms. If invoices go out on 14-day terms and the DSO is 45, clients are paying an average of 31 days late. If terms are net 30 and DSO is 38, the gap is smaller but still present. Whatever the terms, DSO reveals how closely actual collection behaviour tracks the agreed structure.

The arithmetic of improvement is direct. Reducing DSO by 10 days on $4 million in annual revenue releases roughly $110,000 from the receivables balance. That money is already owed. It is sitting in a client’s bank account rather than the business’s, and no new work needs to be delivered to recover it. It simply needs to be collected.

Three Patterns That Push Days Sales Outstanding Higher

Late invoicing adds time before the payment clock starts. In service businesses particularly, invoicing at month end rather than at completion means the agreed payment terms do not begin until weeks after the work was delivered. A project finished on the first of June and invoiced on the last gives the client their standard 30 days from that point rather than from the date of delivery.

Terms that are generous, or that are agreed but not enforced in practice, produce a similar effect. Some industries have settled into customs around payment timing that are considerably more favourable for the buyer than for the seller. These customs often exist simply because no one has formally revisited them. Reviewing whether terms reflect a genuine commercial requirement or an unchallenged habit is worth doing before accepting them as fixed.

The absence of a systematic collections process is the most common explanation for DSO drifting upward in growing businesses. In the early stages, every client relationship is managed personally and overdue accounts are noticed quickly. As the client base widens and the owner’s attention shifts toward delivery and growth, the informal approach fails to scale. Some accounts are followed up, others slip, and DSO rises without any single decision to let it happen.

What the Receivables Balance Means for the New Financial Year

The accounts receivable balance on June 30 does not arrive as cash on July 1. It arrives over the following weeks at the pace of the current DSO. For a business with 40-day DSO and $350,000 in receivables on June 30, the bulk of that cash lands in the second week of August. July begins from whatever the opening bank balance is, not from a combination of that balance and outstanding invoices.

July carries its own obligations: superannuation for the April to June quarter falls due on 28 July, award wage increases from the first full pay period of the new financial year flow into early payrolls, and the new year’s revenue is still building its rhythm. A receivables balance that is higher than it needs to be at June 30 means a longer wait before any of that relief arrives.

A focused collection effort in the next two weeks, targeted at accounts sitting beyond the agreed payment terms, typically shifts the receivables balance meaningfully before the financial year closes. The priority list is simple: identify every account older than the agreed terms, start with the largest balances outstanding, and make direct contact rather than sending an automated reminder. Most overdue accounts, in the pattern we see across owner-led businesses, are overdue because no one has specifically asked for payment recently.

A Working Capital Unlock maps the full picture of trapped cash across debtors, inventory, WIP, and supplier terms, producing a prioritised action list for each item. For businesses where the debtors ledger is the main source of working capital pressure, a Debtor and Collections Reset restructures the invoicing cycle, payment terms, and the follow-up process so that collections runs as a system rather than as a reaction to cash pressure.

ProfitPulse works with owner-led businesses across Queensland and NSW at this point in the calendar. If the June 30 receivables balance has not been mapped against the obligations it will need to fund in July, building that picture now is the most direct cash flow work available before the financial year closes. Book a complimentary 45-minute discovery call with ProfitPulse.

Frequently asked questions

What is Days Sales Outstanding and how do I calculate it for my business?

Days Sales Outstanding measures the average number of days between issuing an invoice and receiving payment. To calculate it, divide your current accounts receivable balance by your average monthly revenue and multiply by 30. A business with $500,000 in receivables and $333,000 in monthly revenue has a DSO of approximately 45 days. Comparing that figure to your payment terms reveals the size of the gap between what you invoice and what clients actually pay on time.

What is a reasonable Days Sales Outstanding for an Australian small business?

In most service-based Australian SMEs, a DSO below 35 days is considered strong. Between 35 and 50 days is common but improvable. Above 60 days typically indicates a systemic issue with the invoicing or collections process rather than a timing quirk. Retail businesses often carry lower DSO because payment is collected at point of sale. Service businesses and B2B operators, where invoicing and payment are separated by agreed terms and a follow-up process, are where DSO most commonly drifts upward without being noticed.

How much cash would reducing my Days Sales Outstanding actually release?

Multiply your annual revenue by the number of days you want to reduce DSO, then divide by 365. A business doing $3 million annually that reduces DSO by 10 days releases approximately $82,000. At $5 million, the same 10-day improvement releases around $137,000. This is cash already owed rather than new revenue. It becomes available when collections run faster, not when the business invoices more. The improvement compounds year on year because a lower DSO baseline carries forward into each new period.

Why do clients pay late and what can I do about it in my Australian business?

Most late payments happen because the buyer’s payment cycle is slower than the seller’s billing process, because there is no systematic follow-up after the due date, or because payment terms were never specifically discussed and the buyer applies their own default timing. The most effective action is direct personal contact after the due date passes, starting with the largest overdue balances. A structured follow-up workflow that escalates from automated reminders to personal calls within a consistent timeframe prevents individual accounts from slipping into extended arrears.

What is a Working Capital Unlock and how does it help owner-led businesses?

A Working Capital Unlock is a four-week project that maps where cash is trapped across a business: debtors, inventory, WIP, supplier payment terms, and bank facilities. It produces a prioritised action list to release each item. For most service businesses, the debtors ledger is the primary source of trapped cash, representing weeks of revenue already earned but not yet collected. A Working Capital Unlock builds the full picture and ranks the most valuable actions by dollar impact.

What is the most effective way to collect overdue invoices before June 30?

Start with an aged debtors report from your accounting system and identify every account where payment is overdue against the agreed terms. Prioritise by dollar value rather than by age. Make direct personal contact with the relevant decision-maker for each large outstanding balance rather than sending an automated reminder. A brief call confirming the expected payment date typically moves an invoice to the front of the payer’s queue. Most businesses find two weeks of focused effort, starting now, produces a meaningful shift before the financial year closes.

How does a fractional CFO help with debtors and cash flow management for Australian SMEs?

For business owners managing delivery, client relationships, and financial administration simultaneously, a fractional CFO arrangement installs the monthly DSO tracking, collections escalation process, and working capital monitoring that most owner-led businesses intend to build but rarely find time to run consistently. Keeping DSO inside a target range month to month prevents the gradual drift that builds a large receivables balance across a full financial year, before it becomes a June 30 problem to fix in a hurry.

Leave a Reply